Navigating Economic Changes Under Trump

Welcome to the new age of financial awareness where understanding the economy and investment is more crucial than ever. Picture this: you’re sitting at your kitchen table, coffee in hand, scanning through headlines that make your head spin. Amidst all the noise, a voice whispers, 'Now’s the time to take control of your financial future.' Join me as we break down the trends affecting your wallet and explore actionable strategies to ensure you thrive in these uncertain times.

Understanding Corporate Influence and Investment Disparities

In today's financial landscape, understanding the role of corporations and their influence on investment opportunities is crucial. The corporate world often prioritizes profit over the well-being of lower-income families. This creates a significant gap in investment opportunities, leading to disparities in wealth accumulation.

1. Exploration of Corporate Tax Cuts and Their Implications

Corporate tax cuts are often touted as a means to stimulate economic growth. But what does this really mean for the average person? When corporations receive tax breaks, they are likely to reinvest that money into their operations. This can lead to job creation and higher wages, but the benefits are not always evenly distributed. Often, the wealth generated from these tax cuts primarily benefits shareholders and executives rather than the workers.

As corporations focus on maximizing profits, lower-income families may find it increasingly difficult to invest. The question arises: how can these families build wealth when they face such financial constraints?

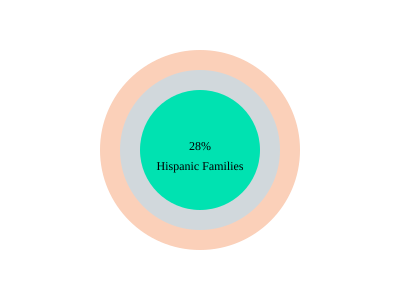

2. Statistics on Stock Ownership by Socioeconomic Class

Investment rates vary significantly across different socioeconomic classes. The statistics speak volumes:

| Demographic | Percentage of Stock Ownership |

|---|---|

| White Families | 66% |

| Black Families | 39% |

| Hispanic Families | 28% |

This table clearly illustrates the disparities in stock ownership among different racial demographics. The gap in investment opportunities is alarming and raises questions about equity in wealth accumulation.

3. The Link Between Socioeconomic Status and Investment Capacity

Socioeconomic status plays a critical role in determining an individual's capacity to invest. Those in higher income brackets are more likely to have disposable income to allocate toward investments. Conversely, families struggling to meet basic needs often have little to no money left for investing.

When basic needs like food, shelter, and healthcare take precedence, investing becomes a distant thought. This leads to a cycle where the rich get richer, while those in lower-income brackets remain stagnant. It's a troubling reality that many face.

4. Expectations for Growing Wealth Through Investing

Many people believe that investing is a surefire way to grow wealth. However, the reality is more complex. For those who have the means to invest, the potential for wealth accumulation is significant. But what about those who can't even afford to start?

Vivian Two aptly states,

"Investing is not just for the rich. It's a necessity for anyone looking to secure their future."This highlights the importance of making investing accessible to everyone, regardless of their financial situation.

5. Reasons Behind Significant Investment Disparities Among Racial Groups

Investment disparities among racial groups can be attributed to various factors, including historical injustices, access to education, and financial literacy. For example, communities of color have often faced systemic barriers that limit their ability to invest.

When families are not educated about investment opportunities or lack access to resources, they miss out on the chance to accumulate wealth. Additionally, cultural factors may also play a role in how different communities view investing. This can lead to a lack of participation in the stock market, perpetuating the cycle of poverty.

6. Examples of Wealth Accumulation Through Investment Practices

Despite the challenges, there are numerous examples of individuals who have successfully built wealth through smart investment practices. They often start small, using tools like robo-advisors to create diversified portfolios. By investing early and consistently, they take advantage of compound interest and market growth.

Moreover, educating oneself about investment strategies can empower individuals to make informed decisions. Whether through online courses, community workshops, or financial advisors, there are resources available to help bridge the knowledge gap.

Investment Ownership by Racial Demographics

The disparities in stock ownership among different racial groups are stark. The following chart illustrates the percentage of stock ownership:

This pie chart visually represents the disparities in stock ownership across different racial demographics. The significant gap in investment participation is a pressing issue that needs to be addressed.

In conclusion, the influence of corporations and the disparities in investment opportunities highlight the importance of financial literacy and accessibility. As the financial landscape continues to evolve, it is crucial for individuals from all backgrounds to understand their investment options and take proactive steps toward wealth accumulation.

Childcare Costs: Navigating Financial Assistance Options

Childcare can be a significant financial burden for many families. With the rising costs of living, understanding the options for financial assistance is crucial. One of the most impactful proposals on the table is the potential change to the child tax credit.

Overview of Trump’s Proposed Changes to the Child Tax Credit

During his campaign, Trump suggested expanding the child tax credit. Currently, the child tax credit stands at $2,000 per child. However, there are proposals that could increase this amount to as much as $5,000.

| Current Child Tax Credit | Potential New Proposals |

|---|---|

| $2,000 | $5,000 |

Such changes could provide much-needed relief for working families struggling to afford childcare. But until these proposals are enacted, families must navigate the current system.

The Importance of Financial Literacy in Childcare Budgeting

Financial literacy is essential when it comes to budgeting for childcare. Families must understand their income, expenses, and the various financial assistance options available. Without this knowledge, they may miss out on opportunities to save money.

As Vivian Two eloquently puts it,

“Childcare is an essential expense that requires strategic financial planning to manage effectively.”This means not only knowing how much things cost but also understanding how to budget for these expenses.

Possible Alternatives Like Dependent Care FSAs

One effective way to manage childcare costs is through a dependent care flexible spending account (FSA). This allows families to set aside pre-tax money to pay for childcare expenses. By using pre-tax dollars, families can effectively reduce their taxable income, leading to potential tax savings.

- Dependent care FSAs can be used for various childcare services.

- They can also cover expenses related to caring for elderly dependents.

- Families should check if their employer offers this benefit.

Implications of Childcare Costs for Working Families

Childcare costs can have profound implications for working families. High expenses can limit parents' ability to work or force them to take lower-paying jobs. This is especially true for single parents or families with multiple children.

Moreover, the lack of affordable childcare options can lead to increased stress and financial strain. Families may find themselves making difficult choices between work and caring for their children.

Steps to Contact Local Representatives for Childcare Support

Advocacy is crucial for families needing childcare support. Contacting local representatives can help ensure that childcare remains a priority in policy discussions. Here are steps to take:

- Identify your local representatives.

- Draft a clear message outlining your concerns about childcare costs.

- Share personal stories to illustrate the impact of these costs on your family.

- Follow up to ensure your message is received and considered.

Creative Strategies for Managing Childcare Expenses

In addition to financial assistance programs, families can adopt creative strategies to manage childcare expenses. Here are a few ideas:

- Consider sharing childcare duties with other families.

- Look for community resources or programs that offer subsidized childcare.

- Explore flexible work arrangements to reduce the need for childcare.

By being proactive and exploring various options, families can better manage their childcare expenses. Financial literacy and awareness of available resources are key components in navigating this challenging landscape.

Visualizing Childcare Costs

To better understand the implications of childcare costs, a bar chart can illustrate the potential financial impact across different states or regions. This visualization can help families see where they stand in comparison to others and motivate them to seek assistance.

Understanding these costs and how they vary can empower families to make informed decisions about their childcare options. It is essential to stay informed and proactive in seeking financial assistance and managing expenses.

Social Security: Reevaluating Retirement Planning

In the current financial landscape, retirement planning is more crucial than ever. With changes in government policies and economic forecasts, individuals need to take a proactive approach. One of the pressing issues is the future of Social Security. Many Americans rely on it as a financial safety net. But is it enough?

Trump's Stance on Social Security

Former President Donald Trump made a commitment to preserve Social Security benefits. He emphasized this during his campaign, promising not to cut into the budget. However, his contradictory statements raised concerns. For instance, he suggested eliminating federal taxes on Social Security benefits. This could potentially deplete the fund further. The paradox lies in the fact that while he aims to protect Social Security, his policies might undermine it.

Statistics on Social Security Fund Projections

According to the Committee for a Responsible Federal Budget, the Social Security fund is projected to run dry by 2031. This alarming date has significant implications for future retirees. Many Americans expect to rely on Social Security for their retirement. However, the reality is that the fund's sustainability is in jeopardy.

| Projected Social Security Fund Depletion Date | Percentage of Americans Expecting to Rely on Social Security |

|---|---|

| 2031 | XX% |

Understanding the Risks of Relying Solely on Social Security

Relying solely on Social Security for retirement is a gamble. As Vivian Two aptly states,

"Relying on Social Security alone for retirement is a gamble that could cost you your future."This highlights the risks involved. Individuals must understand that Social Security was never designed to be the only source of retirement income. It is meant to supplement personal savings and investments.

Alternative Retirement Plans to Consider

- 401(k) Plans: These employer-sponsored retirement accounts allow individuals to save pre-tax income, reducing their taxable income.

- Roth IRA: This is an after-tax retirement account that allows for tax-free withdrawals in retirement.

- Traditional IRA: Similar to a 401(k), contributions may be tax-deductible, but withdrawals are taxed in retirement.

- Catch-Up Contributions: For those over 50, catch-up contributions can help bolster retirement savings.

Encouragement for Increasing Personal Retirement Contributions

It is imperative for individuals to increase personal retirement contributions. The earlier one starts saving, the better. Time is a powerful ally when it comes to compound interest. Financial literacy is key. Individuals should educate themselves on various investment options and strategies.

Anecdote on Planning Retirement Beyond Government Benefits

Consider the story of Sarah, a 55-year-old woman who has been contributing to her 401(k) for over 20 years. She also opened a Roth IRA last year. Sarah understands that Social Security might not be enough to sustain her lifestyle in retirement. By diversifying her savings, she feels more secure. She plans to travel and enjoy her golden years without financial stress. Sarah's proactive approach serves as a model for others.

Addressing the Paradox of Social Security Funding and Demographic Shifts

The paradox of Social Security funding is largely tied to demographic shifts. The aging population is growing, while the birth rate is declining. Fewer workers are contributing to the fund, while more individuals are drawing benefits. This imbalance raises concerns about the future viability of Social Security. Younger generations must recognize this reality and plan accordingly.

Insights on Catch-Up Contributions for Those Over 50

For individuals over 50, catch-up contributions can significantly boost retirement savings. These additional contributions are a vital tool for those who may feel behind in their retirement planning. It's an opportunity to increase savings and secure a more comfortable future.

Conclusion

In summary, the future of Social Security is uncertain. Individuals must take personal responsibility for their retirement planning. Relying solely on government benefits is risky. By diversifying savings and increasing contributions, one can create a more secure financial future. The time to act is now.

The Reality of Tariffs and Consumer Prices

When it comes to the economy, few topics stir as much debate as tariffs. But what exactly are they? Simply put, tariffs are taxes imposed on imported goods. They are designed to make foreign products more expensive, encouraging consumers to buy domestic alternatives. However, this well-intentioned policy comes with unintended consequences, particularly for low-income families.

Understanding Tariffs as a Form of Taxation

Tariffs are often misunderstood. Many people think they are just a trade tool used to punish other countries, but they are, at their core, a form of taxation. When tariffs increase, the costs are not absorbed by foreign manufacturers; they are passed down to consumers. This means that American families end up paying more for everyday items.

"Tariffs are taxes we pay—think about who really bears the burden of those costs." - Vivian Two

The Misconception of Tariffs Benefiting Local Consumers

Some argue that tariffs benefit local consumers by promoting American-made products. However, this perspective overlooks a critical reality. Just because a product is labeled as "Made in America" does not mean it is entirely sourced from the U.S. In fact, many goods are assembled in America using parts from various countries. When tariffs raise prices on imported components, the cost is ultimately passed on to consumers, even for domestically produced goods.

How Tariffs Impact Low-Income Families Specifically

Low-income families are often hit hardest by tariff increases. Why? Because these families spend a larger percentage of their income on essential goods. When prices rise due to tariffs, it can lead to a significant strain on their budgets. For example, if the price of basic necessities increases, these families may have to make tough choices about what to buy.

Examples of Goods Affected by Tariff Increases

- Electronics: Many popular gadgets and devices are manufactured overseas.

- Clothing: Fast fashion brands often source materials from countries with cheaper labor.

- Food Products: Items like coffee and certain fruits are imported from other countries.

Each of these categories can see price hikes that disproportionately affect those with tighter budgets.

Advice for Consumers on Budgeting Amidst Potential Price Hikes

With the reality of tariffs looming, consumers need to be proactive. Here are some budgeting tips:

- Track Spending: Keep a close eye on where your money goes each month.

- Shop Smart: Look for sales and consider bulk buying to save on essentials.

- Prioritize Needs Over Wants: Focus on what is necessary for your household.

By being mindful of spending, families can better navigate the financial strain that tariffs may cause.

Discussion on How Inflation Can Cut Household Budgets

Inflation can further exacerbate the impact of tariffs. As prices rise, households find their budgets stretched thinner. This is particularly concerning for families already living paycheck to paycheck. It may lead to a situation where families have to cut back on essential items, further impacting their quality of life.

In light of these economic challenges, it's crucial for families to engage in financial planning. Understanding how tariffs and inflation interact can help individuals make informed decisions about their spending and saving habits.

Expected Price Increases Due to Tariffs

| Category | Expected Price Increase |

|---|---|

| Imported Goods | XX% |

| Consumer Spending Impact | XX% |

The effects of tariffs echo through markets, disproportionately affecting those at the bottom of the income spectrum. Understanding this reality is crucial for consumers, especially those with limited financial flexibility.

As families continue to face rising costs, the importance of financial literacy and planning cannot be overstated. By preparing for potential price hikes, families can better weather the storm of economic uncertainty.

Taxes and Their Broader Economic Implications

Taxes are a topic that stirs strong emotions. They affect everyone, but the impact varies widely across different income groups. The reality is, tax policy can create a stark dichotomy. Tax cuts often favor the wealthy, while lower-income households bear the brunt of tax increases. This imbalance raises questions about fairness and economic justice.

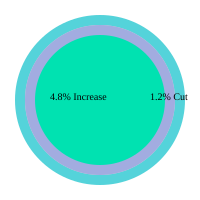

The Dichotomy of Tax Cuts Favoring the Wealthy

When tax cuts are implemented, they frequently benefit the top earners disproportionately. This trend can exacerbate income inequality. For instance, the richest 1% may receive a tax cut of 1.2%, while the lowest income group faces a tax increase of 4.8%. How can this be justified? The numbers speak for themselves.

| Income Group | Tax Change |

|---|---|

| Lowest Income Group | 4.8% Increase |

| Top 1% | 1.2% Cut |

Statistics Illustrating Tax Implications

The statistics tell a compelling story. Lower-income households often find themselves in a precarious financial situation. A tax increase of 4.8% can significantly strain their budgets. In contrast, the top earners receive a mere 1.2% cut. This disparity raises concerns about the sustainability of the middle class.

Strain on Middle and Lower-Income Households

Tax changes can create financial strain for middle and lower-income households. For many families, every dollar counts. A small increase in taxes can mean cutting back on essentials like groceries or healthcare. The question remains: how can policymakers address this imbalance? Personal anecdotes illustrate the real-life impact of these tax changes.

Consider a single mother juggling work and childcare. She relies on every paycheck to make ends meet. When taxes increase, she has to make tough choices. Should she cut back on her children's extracurricular activities? Or forgo necessary healthcare? These decisions are not just numbers on a spreadsheet; they are real-life dilemmas faced by many.

Advocacy and Communication with Legislators

Advocacy plays a crucial role in addressing perceived injustices in tax policy. Individuals must communicate with their legislators to express their concerns. Writing letters, making phone calls, or attending town hall meetings can amplify voices. It’s essential to remind policymakers that tax policies impact real lives.

As Vivian Two aptly stated,

“The real impact of tax changes often falls hardest on those who can least afford it.”This sentiment underscores the need for equitable tax reforms.

Potential Loopholes and Tax Strategies for Individuals

In navigating the complexities of tax policy, individuals can explore potential loopholes and strategies. For example, tax-advantaged accounts like IRAs or 401(k)s can provide some relief. These accounts allow individuals to save for retirement while reducing taxable income. However, it’s crucial to stay informed about changing tax laws to maximize these benefits.

Conclusion

Understanding taxes and advocating for fairer policies is crucial for protecting middle-class interests. The complexities involved in tax policy can have profound effects on individuals' financial decisions. Proactive engagement with policymakers is essential to ensure that tax reforms address the needs of all income groups, not just the wealthy.

Visualizing Tax Burden Distribution

In conclusion, taxes are more than just numbers; they represent choices that affect lives. The need for fairer tax policies is evident. As individuals, staying informed and engaged can help shape a more equitable economic landscape.

Making Sound Financial Decisions in a Changing Economy

In today's world, where economic shifts are frequent and sometimes unpredictable, making sound financial decisions is more important than ever. Understanding how to navigate personal finances can empower individuals to secure their financial futures. This guide aims to provide practical tips for developing financial literacy and personalized strategies, highlighting the significance of taking initiative in managing personal finances.

1. Tips for Developing Financial Literacy

Financial literacy is the foundation for making informed decisions about money. Here are a few tips to enhance your financial knowledge:

- Educate Yourself: Read books, articles, and blogs focused on personal finance. Knowledge is power.

- Take Courses: Many organizations offer free or low-cost courses on budgeting, investing, and retirement planning.

- Engage with Experts: Attend workshops or webinars led by financial advisors.

- Join Communities: Participating in forums or local groups can provide insights and support.

2. The Significance of Taking Initiative

Taking control of one’s finances is crucial. Relying solely on external sources can lead to missed opportunities. It’s essential to:

- Set Clear Goals: Define what you want to achieve financially, whether it's saving for a house or planning for retirement.

- Track Your Spending: Use apps or spreadsheets to monitor where your money goes.

- Make a Budget: Create a realistic budget that reflects your income and expenses.

3. Using Technology Like Robo-Advisors for Investment

Technology has made investing more accessible. Robo-advisors are automated platforms that manage investments for users. They can be a great entry point for novice investors:

- Easy Setup: Most robo-advisors require a simple questionnaire to assess your financial goals.

- Low Fees: Compared to traditional financial advisors, robo-advisors typically charge lower fees.

- Diversification: They offer a diversified portfolio tailored to your risk tolerance.

"Your financial health is in your hands—now's the time to take control." - Vivian Two

4. Financial Success Stories from Average Individuals

Stories of everyday people achieving financial success can be inspiring. For instance, consider someone who started with minimal savings but, through disciplined budgeting and investing, was able to buy a home and secure a comfortable retirement. These narratives emphasize that anyone can improve their financial situation with the right mindset and actions.

5. Common Pitfalls to Avoid in the Current Economic Climate

It's crucial to remain vigilant and avoid common financial traps:

- Ignoring Debt: High-interest debt can quickly spiral out of control. Prioritize paying it off.

- Overlooking Emergency Funds: Life is unpredictable. Aim to save at least three to six months' worth of expenses.

- Chasing Trends: Avoid impulsive investments based on trends. Research thoroughly before committing funds.

6. Steps to Contact Financial Advisors or Educational Resources

Sometimes, seeking professional advice is necessary. Here’s how to find the right resources:

- Research Advisors: Look for certified financial planners with good reviews.

- Utilize Online Platforms: Websites like NerdWallet and Investopedia offer valuable resources and comparisons of financial advisors.

- Ask for Recommendations: Friends or family can provide insights into their experiences with financial advisors.

Data on Robo-Advisors

Robo-advisors are gaining popularity among investors. Here’s a quick look at some relevant data:

| Metric | Value |

|---|---|

| Percentage of Americans using robo-advisors | XX% |

| Average returns from investments using robo-advisors | XX% |

Chart Data Representation

To visualize the impact of robo-advisors, consider the following chart:

Conclusion

In conclusion, making sound financial decisions in a changing economy requires a proactive approach. By developing financial literacy, taking initiative, and utilizing technology like robo-advisors, individuals can significantly improve their financial health. It’s essential to learn from success stories and avoid common pitfalls. Lastly, seeking professional advice when necessary can provide additional guidance. Remember, your financial future is in your hands, and with the right tools and knowledge, you can navigate any economic landscape.

TL;DR: Economic changes under Trump's administration call for heightened financial awareness. Invest wisely, understand new policies' impacts, and prioritize alternative retirement planning over Social Security. Discover simple steps to improve your financial future today.

Comments

Post a Comment